As plan administrator, you are responsible for administering the plan according to the plan documents and in compliance with the IRS.

Your responsibilities as plan administrator include:

Keeping records of all plan activities

Filing on behalf of the plan as needed, including 1099-Rs and 5500-EZs

Ensuring participant loans, if any, are being paid back in a timely manner

Keeping records of all plan activities

Recordkeeping is one of the main responsibilities of the plan administrator. You will need records of all contributions, distributions, investments, etc.

The Miscellaneous Forms section contains forms that you can complete and keep in your files as plan administrator:

Separate accounts are required by your plan. They must be established for each participant and per type(s) of funds within the plan. They are also helpful for tracking the balances of each type of fund within your 401k.

Filings on behalf of the plan as needed, including 1099-Rs and 5500-EZs

You are also responsible for all filings on behalf of the plan. Depending on the activities and value of your plan, you may be required to file a 1099-R and/or a 5500-EZ:

Ensuring participant loans, if any, are being paid back in a timely manner

If a participant loan is taken from your Solo 401k, you also become loan administrator. You must ensure that all participant loans are being repaid in a timely manner, according to the repayment schedule established at the time of the loan.

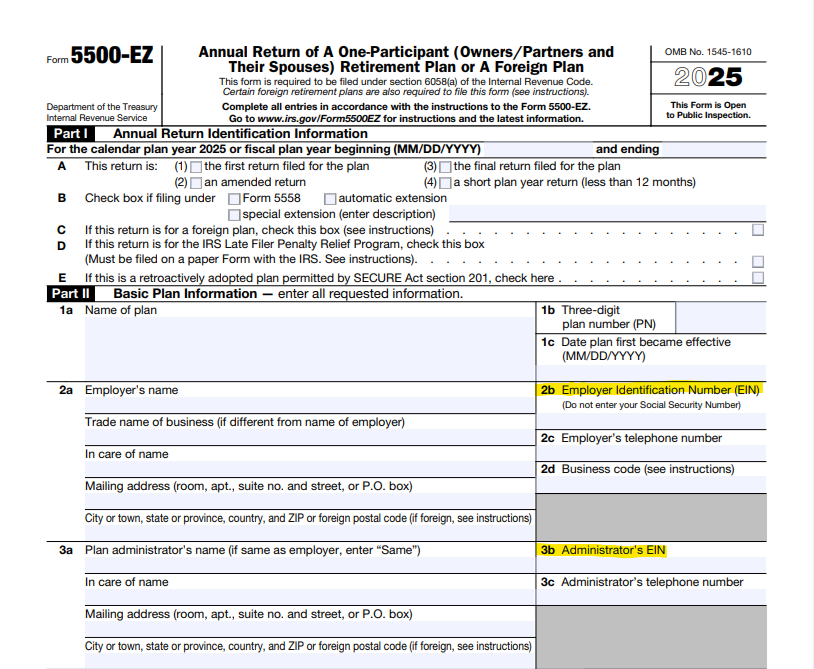

You may be able to obtain a possible extension for filing Form 5500-EZ, but extensions must be obtained before the filing due date. If an extension is obtained, you would mark the appropriate box on Form 5500-EZ, Part I, B.

The due date of Form 5500-EZ filing is:

The last day of the 7th calendar month after the plan year end

This is July 31st, if the plan year end is December 31st

Possible extensions to file Form 5500-EZ include:

Form 5558

You can file for a one-time extension of the Form 5500-EZ deadline by filing Form 5558.

To be granted an extension:

Form 5558 must be filed by the Form 5500-EZ deadline

Form 5558 is for a one-time extension

The extension is up to the 15th day of the 3rd month after the normal Form 5500-EZ filing deadline

Form 5558 instructions and information can be found on the IRS website:

You may also be granted an extension of the Form 5500-EZ deadline if your adopting business has been granted an extension of its federal income tax return, to a date later than the normal Form 5500-EZ deadline.

This extension is automatically granted if all of the following conditions are met:

Your Solo 401k plan year and your adopting business’s tax year are the same, and

Your adopting business has been granted an extension of its federal income tax return, to a date later than the normal Form 5500-EZ deadline, and

A copy of the application for the extension of its federal income tax return is retained with your Solo 401k plan records

To utilize this extension, check “Automatic extension" in Part I, B of Form 5500-EZ.

Other special extensions announced by the IRS

According to the IRS:

The IRS may announce special extensions of time under certain circumstances, such as extensions for Presidentially-declared disasters or for service in, or in support of, the Armed Forces of the United States in a combat zone. If you are relying on one of these announced special extensions, check the “special extension” box on the Form 5500-EZ, Part I, line B, and enter a description of the announced authority for the extension.

The mega backdoor Roth strategy is a way to get more Roth funds into your retirement account. Roth funds are taxed initially but grow tax-free.

The mega backdoor Roth strategy consists of:

Making after-tax contributions to the Solo 401k, and

Converting those after-tax contributions to Roth within the Solo 401k, and

Keeping those Roth funds in the Solo 401k for checkbook-control investing or rolling over the funds into a Roth IRA

The Mega Backdoor Roth strategy offers an alternative to contributing to a Roth IRA directly, which is limited to $7,000 per year by the IRS. Many individuals also do not qualify for a Roth IRA due to their high earnings.

Your Solo 401k with Sense Financial already includes the features which allow you to utilize the mega backdoor Roth strategy.

How it works

Open separate accounts for your Solo 401k to house your after-tax contributions and Roth funds, if you do not have these already

From a banking standpoint, these separate accounts will be identical. Both are in the name of your 401k and using the EIN of your 401k. However, these accounts are established to keep the funds separate from each other and to assist you in your accounting of each type of fund within your 401k. You can assign nicknames to the separate accounts online in order to differentiate them.

Calculate the after-tax contribution based on your self-employment business earnings

Make the after-tax contribution into the 401k account for after-tax contributions

Once that after-tax contribution is in your 401k, immediately convert the funds to Roth and move those funds to the Roth account

Note that the growth on the after-tax contribution is taxable, so you will want to convert the after-tax contribution to Roth immediately after the contribution is made.

Keep those funds within the Roth account of your Solo 401k for checkbook-control investing or roll those funds over to a Roth IRA

The following year, file a 1099-R to document the conversion

How it should be reflected on a 1099-R

In this case, the 1099-R should document the conversion of the after-tax contribution to Roth within your 401k. The Payer is your 401k trust, which is issuing the 1099-R to you, the Recipient.

Payer: your 401k trust

Payer TIN: the EIN of your 401k trust (not the EIN of your adopting business)

Recipient TIN: your SSN

Recipient: you, as an individual

Box 1: Gross distribution: amount that was converted to Roth

Box 2a: Taxable amount: 0.00 if the after-tax funds were converted to Roth immediately. The taxable amount would be 0.00 since the after-tax contribution was not originally claimed as a deduction and was converted to Roth immediately. If the after-tax contribution was not converted to Roth immediately, the growth amount is taxable and should be entered here.

Box 5: Employee contributions/Designated Roth contributions or insurance premiums: amount of the original after-tax contribution. If you converted the after-tax contribution to Roth immediately after making the contribution, this should be the same amount as in Box 1

Box 7: Distribution code: G which indicates a direct rollover (from after-tax to Roth) within the plan, your 401k

When the 1099-R should be filed

The 1099-R is filed in the year following the year in which the Roth conversion was performed (e.g. the 1099-R for 2022 is filed in 2023). There are two deadlines for the 1099-R:

The Payee/recipient copy must be received by January 31st

The electronic copy must be filed with the IRS by March 31st

You are responsible for the filing of the 1099-R by both deadlines.

The IRS has released Form 8915-E and 8915-F for the reporting of CARES Act distribution(s) that were taken in 2020, their repayment, or their inclusion in income.

If you took a CARES Act distribution in 2020, note which form(s) would apply to you:

Form 8915-E is used to report:

If you took a CARES Act distribution in 2020

Form 8915-F is used to report:

Your income in 2021 if you took a CARES Act distribution in 2020 and have been including in your income in equal amounts over 3 years and that 3-year period has not yet lapsed

Your repayments of a CARES Act distribution, if repaying the distribution

Note that repayment of the CARES Act distribution can be done over 3 years, starting with the day after the distribution was received. Repayment(s) can occur through multiple payments or one lump sum payment by the end of those 3 years. If the entire CARES Act distribution is paid back within that time, the distribution will not be taxed.

You will want to request your CPA’s assistance in completing the appropriate form for your situation.

More information on these two forms can also be found at:

I'm getting ready to file Form 5500-EZ and need help calculating the plan assets of my 401k. I used some of the funds for a down payment to purchase an investment property. The rest of the purchase price was financed using a hard money loan. My wife doesn't have any investments at this time, just some cash. How do I calculate the net plan assets?

To calculate the total plan assets of the 401k, add up all assets plus cash for all participants.

Form 5500-EZ is for the entire plan, i.e. for all participants, combined. If the total plan assets exceed $250,000, you are required to file Form 5500-EZ.

If you are performing an in-kind conversion or taking an in-kind distribution of the property (i.e. there is a taxable event), then a third-party licensed appraisal must be obtained to determine the accurate value of the property. The appraisal must be dated as close as possible to the taxable event.

Can you provide guidance on what I'm required to do on the tax/CPA side of things? What should I submit to my accountant for the plan?

Note that we are not qualified to provide tax, legal or investment advice. This information is intended as general guidance only. You should always consult with an experienced tax professional regarding your personal tax situation.

Depending on your activity within your Solo 401k for the year, you may need to submit your records of the following to your CPA:

If you made contributions to your Solo 401k, you will need to report them on the appropriate return(s). See the section on "Report your contributions."

If you performed a Roth conversion, distribution, or defaulted on a participant loan from your Solo 401k, you are responsible to file Form 1099-R on behalf of your plan to report it:

As plan administrator of your Solo 401k, it is your responsibility to maintain the recordkeeping of the plan. This includes the contributions, distributions, investments, etc.

If I file Form 5500-EZ now, does that obligate me to file subsequent 5500-EZ forms for the following years even if the total plan assets are below 250k?

No. Form 5500-EZ is only required if the total plan value is $250,000 or above, as of the end of the plan year.

Filing the form is not required if the total plan value is below $250,000 as of the end of the plan year, even if the form has been filed for the previous year.

The IRS instructions for Form 5500-EZ note:

You do not have to file Form 5500-EZ for the 2025 plan year for a one-participant plan if the total of the plan's assets and the assets of all other one-participant plans maintained by the employer at the end of the 2025 plan year does not exceed $250,000, unless 2025 is the final plan year of the plan.