Can I contribute more than my business has in revenue?

Can I contribute more than my business has in revenue?

Answer:

No. All your contributions (whether pre-tax or Roth) must come from your business earnings.

Can I contribute more than my business has in revenue?

No. All your contributions (whether pre-tax or Roth) must come from your business earnings.

Yes. All your contributions must come from your business profits. You should create a separate designated Roth account for ease of tracking your Roth balance and use the appropriate form to document your contributions. Forms can be accessed here:

Forms to Administer Solo 401k Plan

The Solo 401k participant typically makes annual Solo 401k plan contribution when completing business tax return for the year. As a result, the Solo 401k participant can usually determine her IRC Sec. 404 deduction limits before making her Solo 401k contribution, thus preventing any excess Solo 401k contribution headaches.

10 Percent Penalty and Form 5330: When the Solo 401k participant contributes more than the allowable deduction for a given tax year, he is typically required to pay a 10 percent penalty on the over contribution amount also known as the excess nondeductible contribution amount pursuant to (IRC Sec. 4972). As such, this penalty amount must be reported to the IRS by the plan participant since he is the owner of the business by filing IRS Form 5330, Return of Excise Taxes Related to Employee Benefit Plans, and remit the penalty to the IRS. Please refer to IRC Sec. 404(a)(1)(E) as it details that the amount of the otherwise deductible contribution that exceeds the limitation for any given year shall be carried forward indefinitely and applied to subsequent years.

IMPORTANT: Even though excess nondeductible Solo 401k contributions may be returned to the Solo 401k employer under limited circumstances, the Solo 401k employer runs the risk of incurring substantially greater penalties by taking a reversion of plan contributions. The reversion penalty is typically as high as 50 percent depending on the circumstances pursuant to (IRC Sec. 4980).

When removing excess contributions from a solo 401k plan, you first need to determine the type of contribution being removed. There are 2 (two) types of contributions that apply to a solo 401k plan.

The rules for removing the employee contributions vs the employer profit sharing contributions are different and are discussed below.

Here is what the IRS code says regarding removing Employee Contributions

If the excess salary deferral is not returned on or before April 15 of the following year, the contributing participant must pay income tax on the deferral both in the year of deferral and in the year of distribution. The deferrals are not included as after-tax assets even though they have previously been included in income in the year of deferral (IRC Sec. 402(g)(1) and (Treas. Reg. 1.402(g)-1(e)(8)). The earnings on the excess will be taxed in the year of distribution. Any corrective distribution of less than the entire amount of the excess deferral plus income is treated as a pro rata distribution of excess deferrals and income (IRC Sec. 402(g)(2)(D), Treas. Reg.1.402(g)-1(e)(10)).

For the employer contributions (profit sharing), here is what the rules state:

As the year comes to a close, we'd like to remind you to plan for your contributions to your Solo 401k. In this article, we'll discuss the following questions:

How do I calculate my contributions for this year?

For more information:

How do I actually make contributions to my Solo 401k?

For more information:

When is the deadline to make contributions?

For more information:

Am I required to make annual contributions to my Solo 401k Plan?

Answer:

Contributions are not required every year. However, the plan will not be considered qualified if it appears from surrounding facts and circumstances that the plan was established as a temporary program.

A plan will be considered temporary if:

A plan will be considered permanent as long as substantial contributions are being made occasionally, even if contributions are not made every year. The employer reserves the right to discontinue the profit sharing contributions without jeopardizing its status as a permanent program.

Are there any matching contributions for a Solo 401k?

No. Matching contributions are listed in the Solo 401k Plan as not applicable.

There are no matching contributions because the plan is designed to be as flexible as any retirement plan can be allowed by law in the U.S. This might mean that some years you will make employer contributions and in other years you won’t. This allows the greatest flexibility within the plan. Employer contributions are known as "Profit Sharing". Please review the following link to learn more:

Your Solo 401k requires separate accounts per participant and per type, such as:

Depending on the number of participants and types of funds within your Solo 401k, you will need to establish that number of account(s), when you are ready to fund them.

For example, if you are the only participant and you will be making an employee/elective deferral contribution and an employer/profit sharing contribution, you will open two separate accounts.

This requirement is listed on your Summary Plan Description, page 11.

For checking accounts, you can assign nicknames to distinguish between the accounts. Nicknames should identify the participant and the type of fund within the 401k.

Bank Account Set Up

Separate accounts enables easier accounting for each type. You are required to account for each type of fund within your Solo 401k, including the returns on investments made with that type of fund.

You will need to establish a clear accounting method to keep track of each type of fund. The format for tracking and accounting is up to you. It's best to choose a method that you are already familiar with, such as:

For example, employee/elective deferral contributions cannot be distributed from the plan as an in-service distribution before the participant is age 59 ½. Employer/profit sharing contributions, however, can be distributed as an in-service distribution without age restriction.

Rolling funds out of the Solo 401k

Although there are separate accounts within the 401k, the funds from the separate accounts can be combined for investments.

Using both spouse’s accounts under the same 401k

Can profit sharing contributions to my Solo 401k be made throughout the year, or do I have to wait until the end of the year to make them?

If you and your spouse work in your business together and your spouse stops working in the business, (s)he can still participate in the plan in terms of directing their existing assets in the plan. Your spouse has all the rights of the participant except the ability to make contributions into the plan.

Your spouse does not need to transfer their funds out of the plan and stop being a participant. However, (s)he can not make contributions.

Can you please explain how to make contributions to my 401k from my corporation. Can I get paid by the corporation as an independent contractor via 1099 and then claim the state taxes on my personal return or do I need to do the payroll deductions and submit them to the state?

Since your 401k plan is sponsored by the corporation, all employee elective deferrals must be made through the payroll.

Profit sharing contributions are made by the company and are 100% deductible.

Since you own a corporation you must take reasonable salary, please consult your CPA or tax advisor for details. Be sure to inform your payroll service provider (payroll company or your CPA) that you intend to make contributions into the 401k. Contributions made by the employee must be reflected on the payroll and the funds must be deposited to 401k account within 7 days of payroll.

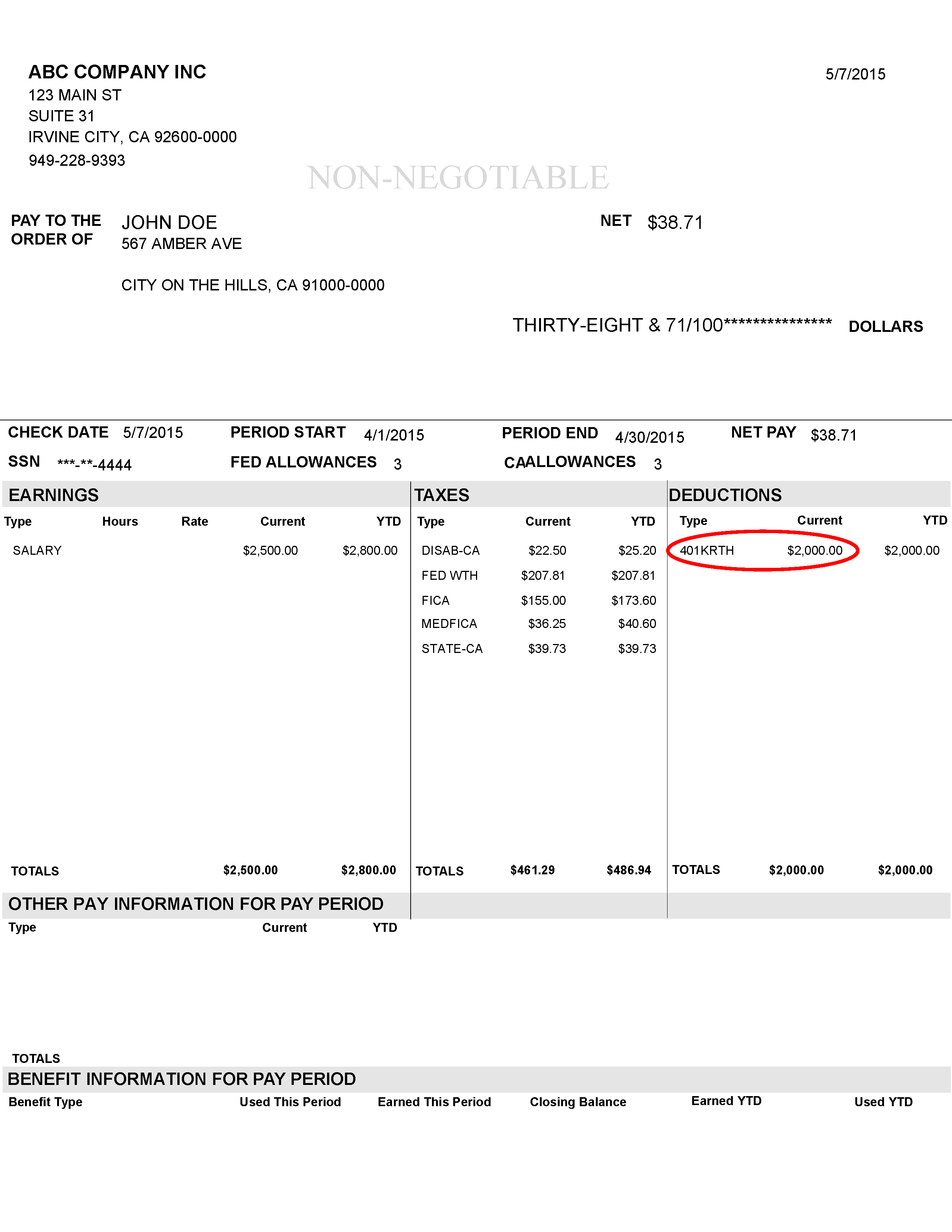

Below is an example of a paystub showing the deduction from wages, into the Roth 401k:

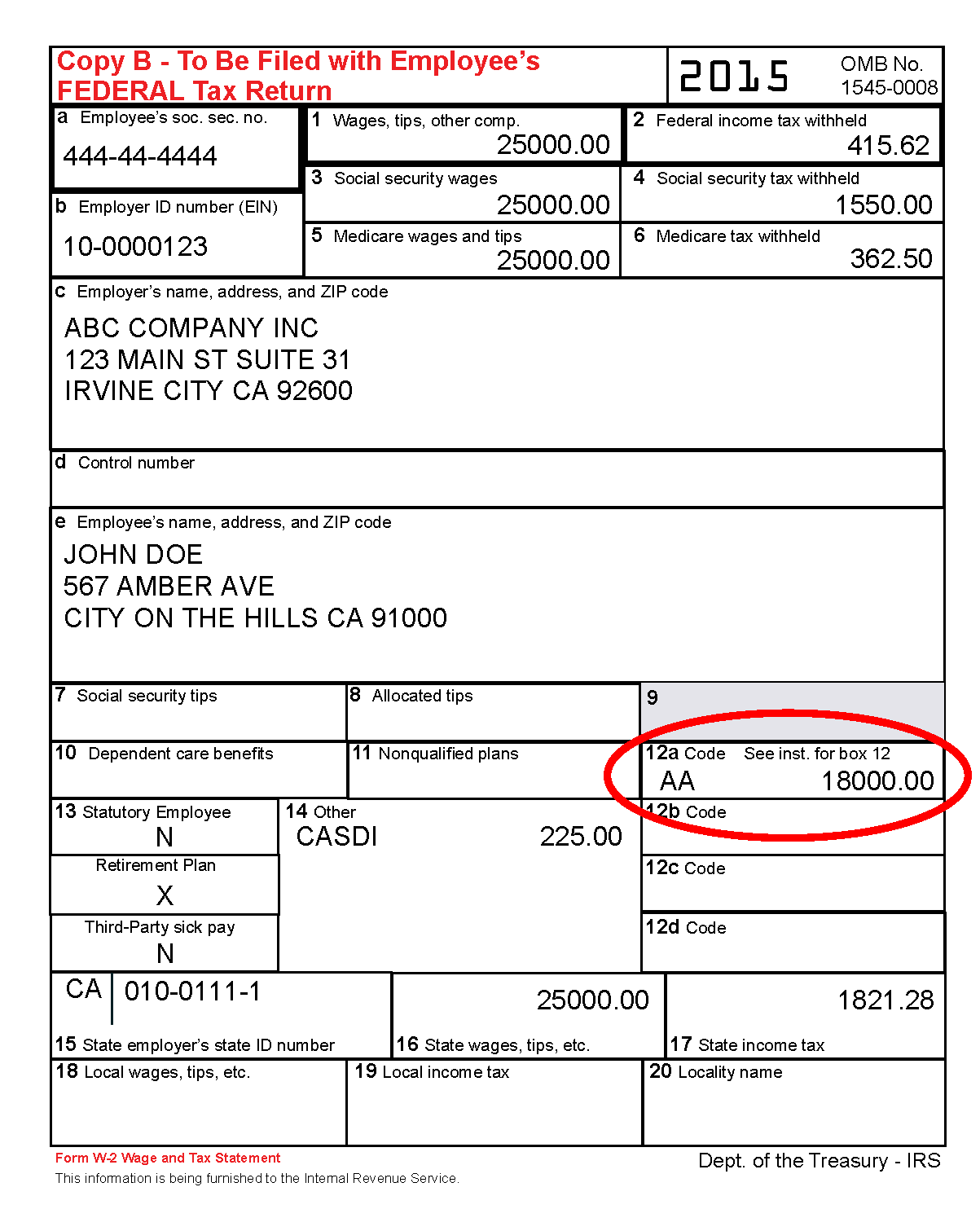

Below is an example of the W2 showing $18,000 contribution made to a Roth 401k in the box 12a:

(In the example below there are Roth contributions (Box 12a code AA). In this case, the amount would be included in box 1. If the deferrals are pre-tax the code used in box 12a would be "D" and then amount in box 1 would be reduced by the amount in box 12a.)